Special feature on reinsurance: Reinsurers' profitability

The second part will be dedicated, among other things, to the rating of reinsurers, the loss experience of natural catastrophe risks and to aviation reinsurance. The issue summary will be completed with an overview of the world's main reinsurance markets. In addition, and as of early November, we will be publishing on the website of Atlas Magazine a directory of leading reinsurers operating in Africa, the Middle East and the world.

Reinsurance profitability

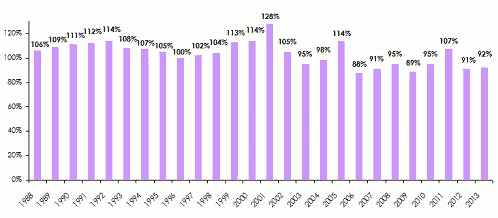

From 1988 to 2002, that is, for over 15 years, combined ratio of non life reinsurance has never been less than 100%, with a peak of 128% in 2001.

In fact, It is only after the catastrophe of World Trade Center in 2001 that the market started recovering truly.

With a record solvency and an average combined ratio 92% for the period 2009 to 2013, reinsurance remains today a sound market to which Standard & Poor's has awarded an "A" rating.

Having become a "safe haven" for many floating funds, the activity is risking to pay dearly for its success. The flow of capacity combined to shrinking demand will trigger as of 2015 a decline in profitability, pushing the market to undertake major restructuring.

For the years 2014 and 2015, deterioration of the combined ratio is very likely. Standard & Poor's is expecting an average ratio of 95% to 100% in 2014

Evolution of non life reinsurance combined ratios: 1988-2013

Source: Standard & Poor’s

Source: Standard & Poor’s

Decrease in the intensity of natural and technical catastrophes

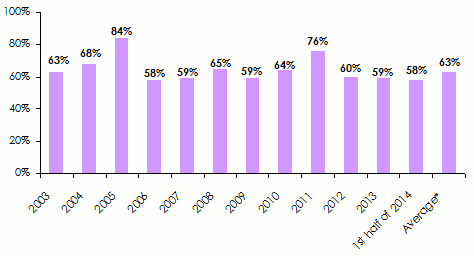

Insured losses related to natural and technical catastrophes, have gone from 129 billion USD in 2011 to 45 billion USD in 2013, far from the average value reported in the previous ten years and which amounted to 61 billion USD.

The events of September 11, 2001 with their peak in claims have forced reinsurers to undertake an overhaul of their business model. Since then, thanks to a return to the fundamentals of insurance, loss experience has been declining. With the exception of 2005 (Katrina disaster) and 2011 (Japan earthquake), the loss ratio was maintained in a range between 58% and 68%.

Evolution of loss ratios: 2003-2013

* Average of the last five years Sources: AM Best, IAIS

* Average of the last five years Sources: AM Best, IAIS

Combined ratio for the first six global reinsurers: 2009-2013

With the exception of 2011, which was bad for the overall market, large reinsurers were able to gain some points with regard to combined ratio. The absence of significant large-scale natural catastrophes has allowed Lloyd's of London to achieve excellent performance. Over the last five years on average, it is Swiss Re which has displayed the lowest combined ratio (90.5%) and Munich Re, the world leader in terms of premium which has brought up the rear with a rate of 98.86%.

| 2009 | 2010 | 2011 | 2012 | 2013 | |

|---|---|---|---|---|---|

Munich Re | 95.80% | 101% | 114.20% | 91.20% | 92.10% |

Swiss Re | 88.30% | 94.20% | 101.60% | 83.10% | 85.30% |

Hannover Re | 96.80% | 98.50% | 104.50% | 96% | 95.10% |

Lloyd’s | 78.40% | 90.30% | 130.60% | 91% | 80.10% |

SCOR | 98.80% | 100% | 104.50% | 94.30% | 93.40% |

Berkshire Hathaway | 92.50% | 92.40% | 99.90% | 99.90% | 86.60% |

Source: AM Best

Evolution of combined ratios in the MENA zone

| Country | 2009 | 2010 | 2011 | 2012 | 2013 | |

|---|---|---|---|---|---|---|

Milli Re | Turkey | 110.5% | 108.5% | 131.1% | 107.8% | 115.1% |

Trust Re | Bahrain | 86.4% | 86.0% | 94.4% | 95.3% | 95.4% |

Qatar Re | Qatar | - | 76.3% | 121.9% | 113.6% | 110.7% |

Arab Ins Group | Bahrain | 98.7% | 104.1% | 108.6% | 96.8% | 99.0% |

Compagnie Centrale de Réassurance | Algeria | 82.6% | 73.1% | 74.2% | 78.2% | 75.8% |

Société Centrale de Réassurance | Morocco | 98.9% | 97.1% | 95.7% | 83.6% | 67.3% |

Kuwait Re | Kuwait | 94.2% | 106.0% | 101.0% | 94.2% | 97.3% |

Saudi Re | Saudi Arabia | 226.2% | 147.6% | 141.9% | 83.6% | 136.8% |

Arab Re | Lebanon | 113.0% | 101.4% | 101.5% | 97.0% | 104.9% |

Tunis Re 1 | Tunisia | 98% | 98% | 108% | 98% | 95.5% |

Gulf Re | United Arab Emirates | 99.2% | 94.5% | 92.4% | 104.1% | 120.9% |

ACR ReTakaful | Bahrain | 76.0% | 87.1% | 191.0% | 177.6% | 176.6% |

Emirates Retakaful | United Arab Emirates | 109.5% | 107.5% | 116.2% | 95.7% | 98.3% |

Total | 100.9% | 89.8% | 113.4% | 98.8% | 99.4% |

1 Net combined ratio, Tunis Re figures Source: AM Best

In the MENA region, publicly-held reinsurers, receiving legal cessions and achieving most of their turnover on their local markets, have exhibited the best combined ratios. This is the case of CCR Algiers and SCR Morocco.

With the exception of Trust Re, whose results remain excellent throughout the entire period, regional reinsurers have volatile loss ratios and often above 100%. The poor performance of retakaful companies is worth noting.

Combined ratios’ evolution of some African reinsures

| 2009 | 2010 | 2011 | 2012 | 2013 | |

|---|---|---|---|---|---|

Ghana Re | - | - | 76.80% | 62% | 80.70% |

Kenya Re | 92% | 86% | 87.8% | 114.10% | 98.70% |

Zep Re | 88.8% | 94.4% | 91.60% | 89.30% | 92.10% |

Africa Re | 88.3% | 83.2% | 84.40% | 86% | 83.10% |

Munich Re Africa | 78.7% | 85.6% | 100% | 103.20% | 86.30% |

Hannover Re Africa | 91.3% | 83.2% | 88.70% | 85.70% | 90.20% |

Sources: Standard & Poor’s, AM Best

Africa remains hardly exposed to natural catastrophes. Non life markets are still dominated by motor, health and fire. Only large risks associated with the cotton industry, textile, energy and petrochemicals can change the loss ratio.