MENA zone reinsurance market: 2018 renewals

|

Over the last decades, the economies of the countries concerned have greatly benefited from the income reaped from the sale of raw materials, foreign investment and the emergence of a middle class. Insurance wise, local authorities have gradually initiated measures designed to bring their markets closer to international standards. Particular attention has, therefore, been paid to prudential rules and premium retention.

This economic and structural progress is unfortunately hindered by political instability, the devaluation of currencies and the extreme diplomatic tension that has recently set in. Falling oil prices make the situation worse, pulling economies downwards.

It is therefore with new constraints that reinsurers are approaching the next renewal in this troubled area.

MENA zone reinsurance market: economic and political situation

Reinsurers in MENA zone have long benefited from the endogenous and steady growth of local insurance markets. Thanks to the good performance of the region's economies and despite stiff competition, growth prospects are higher than those of other markets.

The economic gap that separates MENA zone from developed countries is gradually bridging thanks to a higher development dynamic. The sector’s deregulation and the adjustment of legislation, particularly with the introduction of compulsory coverages, brought about new momentum. Moreover, apart from Turkey, Iran and Algeria, exposure to natural catastrophes is relatively low. This is the case of the countries bordering the southern Persian Gulf, which therefore constitutes a particularly interesting alternative for reinsurers keen on diversifying their portfolios. These attractions have, to date, enabled the development of local financial centers such as Dubai International Financial Center (DIFC) and Qatar Financial Center (QFC).

Yet this economic prosperity in the Gulf countries is bumping into rocky times. Indeed, these countries are undergoing severe economic and political pressure. Long-standing regional conflicts have only picked up, particularly in Yemen while relations between Iran and Saudi Arabia have deteriorated. At the same time, Qatar is entering into an unprecedented diplomatic conflict with all neighboring Arab countries.

With a declining price of oil barrels, producer countries can only see their earnings melt away. This new situation weighs heavily on public finances. The States concerned are compelled to take drastic measures to contain the effects of their shrinking resources. The introduction of austerity measures limits investment in infrastructure, the historic engine of growth. At the same time, the salaries of civil servants are reduced while the employment of foreigners remains limited.

Read also | MENA insurance market in 2018

Major reinsurers of the MENA zone

Dubai International Financial Center @Jackardsiffant, CC BY 3.0 Dubai International Financial Center @Jackardsiffant, CC BY 3.0 |

Approximately, twenty local reinsurers are active in the MENA region. Their underwriting capacity has steadily increased with the growing complexity of risks and the increase in insured values.

Over time, they have come to grasp ways of tapping into modern tools and local know-how. Despite this progress, the investment of large-scale risks continues to be made with international reinsurers. The latter bring their experience and their mastery of modeling techniques as well as a better ability to pool risks. The substantial capabilities they have and rating requirements from insurers and multinationals surely provide them with competitive edge.

Major reinsurers operating in the MENA zone

in millions USD| Country | Gross written premiums 2016 | |

|---|---|---|

Trust Re | Bahrain | 481.7 |

Saudi Re | Saudi Arabia | 262.8 |

Milli Re | Turkey | 258.7 |

Compagnie Centrale de Réassurance | Algeria | 247.1 |

Arig | Bahrain | 245.4 |

Société Centrale de Réassurance | Morocco | 236.1 |

IGI | United Arab Emirates | 231.4 |

Hannover ReTakaful | Bahrain | 160.8 |

Kuwait Re | Kuwait | 96.3 |

Arab Re | Lebanon | 66.5 |

Emirates Re | United Arab Emirates | 63.9 |

Tunis Re | Tunisia | 48.5 |

Iraq Re | Iraq | 25.8 |

Oman Re | Oman | 23.7 |

Mamda Ré | Morocco | 9.2 |

Arab Union Re | Syria | 3.3 |

ACR ReTakaful | Bahrain | 1.3 |

MENA zone reinsurance market : access to new markets as a source of diversification

The set of factors generating economic and political instability previously stated has a negative impact on the entire region, exacerbating the volatility of the market results.

Local reinsurers who rely heavily on domestic markets are trying to amplify their diversification by including Africa or Asia in order to contain any fluctuations in their turnover. This strategy limits their dependence on the markets of the Gulf and North Africa where competition is stiff even as the frequency of claims continues to increase. For reinsurers in the MENA zone, Asia and Africa are alternatives exhibiting substantial growth potential while rates are deemed more adequate than those in force in their own market.

Some regional reinsurers underwrite natural catastrophes risks by controlling their engagements through Lloyd's syndicates to which they have access, a move particularly true for floods risk.

MENA zone reinsurers' results

The diversity of underwriting strategies pursued by reinsurers in the MENA zone has shaped very different portfolio profiles.

Most of the underwritten revenues come from proportional business. The non-proportional acceptances remain confined to the motor class of business, developing slowly in the damage to property class.

It is worth noting that some reinsurers benefit from legal assignments. This diversity of portfolio profiles has entailed disparate performance.

MENA zone reinsurers: technical performance in 2016

| Loss ratio in % | Combined ratio in % | ||||||||

|---|---|---|---|---|---|---|---|---|---|

Company | Country | 2014 | 2015 | 2016 | 5-year average | 2014 | 2015 | 2016 | 5-year average |

Trust Re | Bahrain | 67 | 65 | 68 | 66 | 97 | 96 | 96 | 96 |

Saudi Re | Saudi Arabia | 75 | 58 | 78 | 77 | 107 | 80 | 103 | 104 |

Milli Re | Turkey | 83 | 88 | 77 | 78 | 116 | 120 | 111 | 110 |

Compagnie Centrale de Réassurance | Algeria | 40 | 47 | 51 | 47 | 72 | 79 | 81 | 77 |

Arig | Bahrain | 67 | 66 | 61 | 63 | 104 | 109 | 93 | 100 |

Société Centrale de Réassurance | Morocco | 55 | 75 | 73 | 53 | 95 | 87 | 87 | 84 |

IGI | United Arab Emirates | 53 | 44 | 45 | NA | 87% | 84 | 87 | NA |

Hannover ReTakaful | Bahrain | 84 | 70 | 70 | 73 | 118 | 100 | 102 | 107 |

Kuwait Re | Kuwait | 68 | 60 | 65 | 66 | 106 | 95 | 103 | 99 |

Arab Re | Lebanon | 78 | 69 | 73 | 72 | 113 | 99 | 109 | 105 |

Emirates Re | United Arab Emirates | 67 | 64 | 104 | 74 | 96 | 97 | 176 | 111 |

Tunis Re | Tunisia | 58 | 51 | 53 | 54 | 100 | 91 | 91 | 96 |

Oman Re | Oman | 170 | 98 | 55 | 98 | 232 | 152 | 101 | 148 |

ND : not available

The fall in insurance rates coupled with the increase in the frequency of claims has considerably strained non life reinsurers. Few players have managed to maintain positive operating results. A high number of combined ratios exceeds 100%. The decline in underwriting results stems not from commission rates, which have remained broadly stable, but from loss ratios well above the international average.

Modest premium volumes reported by life reinsurance remain too low to offset the negative results of the non life business.

Deteriorating exchange rates in many Gulf and Maghreb countries coupled with inflation have also contributed to lower profits.

The current political instability that characterizes the region could aggravate monetary instability, hence the likelihood of further deteriorating results.

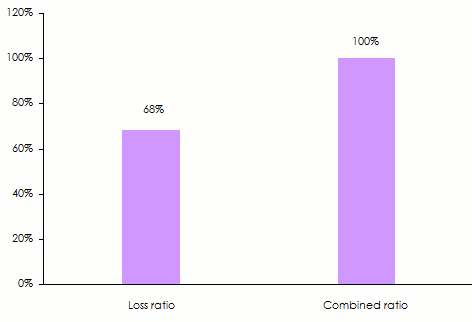

MENA zone reinsurance market: Average of the last five years (2012-2016) of loss ratios and combined ratios

Source: Best’s Special Report, AM Best

Source: Best’s Special Report, AM BestThe lingering losses reported by the fire class of business have weighed heavily on the results. Competition between traditional regional players is exacerbated by the influx of new capacity and the appetite of international reinsurers.

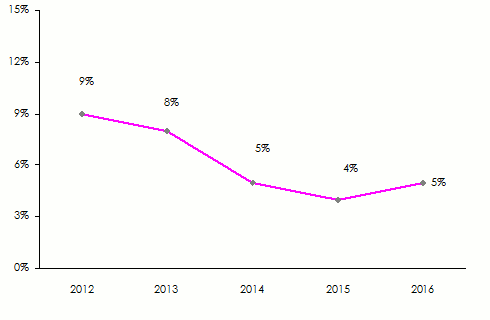

In the meantime, return on investment has been affected by low interest rates. As a result, return on equity was by and large halved between 2012 and 2016:

Return on equity of the MENA zone reinsurers: 2012-2016

Source: Best’s Special Report, AM Best

Source: Best’s Special Report, AM BestRating of the main reinsurers

| AM Best | Standard & Poor’s | ||||

|---|---|---|---|---|---|

Company | Country | Rating | Outlook | Rating | Outlook |

Trust Re | Bahrain | A- | Stable | A- | Stable |

Saudi Re | Saudi Arabia | - | - | BBB+ | Stable |

Milli Re | Turkey | B+ | Negative | - | - |

Compagnie Centrale de Réassurance | Algeria | B+ | Stable | - | - |

Arig | Bahrain | A- | Stable | - | - |

Société Centrale de Réassurance | Morocco | B++ | Stable | BBB- | Stable |

IGI | United Arab Emirates | A- | Stable | A- | Stable |

Hannover ReTakaful | Bahrain | - | - | A+ | Stable |

Kuwait Re | Kuwait | A- | Stable | - | - |

Arab Re | Lebanon | B+ | Stable | - | - |

Emirates Re | United Arab Emirates | B++ | Positive | - | - |

Tunis Re | Tunisia | B+ | Stable | - | - |

Oman Re | Oman | B+ | Stable | - | - |

ACR ReTakaful | Bahrain | B++ | Stable | - | - |

MENA zone reinsurance renewals: the 2018 trends

In non life reinsurance, the MENA region has a turnover of around 13 billion USD, or nearly 6% of the sector's global premiums. Following a large number of major claims in the fire, engineering and energy classes, reinsurers' underwriting profits have constantly decreased.

Fierce tariff competition on basic business has had a direct impact on the results of the proportional treaties.

Casablanca, Morocco © Karel291, CC BY 3.0 Casablanca, Morocco © Karel291, CC BY 3.0 |

The insurance barometer published in 2016 highlights deep concerns expressed by professionals in the sector, the majority of whom expect firmer terms and conditions for the next renewal. As for now, the issue is not yet over a clear increase in tariffs, but over the likelihood of sticking to existing reinsurance conditions.

Insurers in the Middle East and the Maghreb are selling on average 29% of their premiums to reinsurers, a rate that is approximately four times higher than global average. A good capitalization is likely to allow direct companies to limit their cessions, which is likely, in fact, to only aggravate competition among reinsurers in search of maintaining their market shares.