Special Reinsurance, the market in 2015

The market status by the end of 2015

Licence standard de Fotolia Licence standard de Fotolia |

In terms of loss experience, the year 2015 has been relatively mild on insurers and reinsurers who sustained very few major catastrophes. Despite this piece of good news, rating agencies are maintaining their negative outlooks for reinsurance. A series of unfavorable factors continues to penalize the business with little signs for the appraisals made by the agencies to change in 2016.

For the next year, the market players will be facing the same challenges as in 2015, that is, a deteriorated economic environment, a sluggish growth, an abundance in capacity, poor financial yields, stagnant demand, and an increasingly exacerbated competition. Reinsurers can but cope in order to survive.

Abundance of capacity

The reinsurance market has been strained by the abundance of capacity from different sources such as:

The proliferation of alternative capitals

Reinsurance continues to attract alternative capitals whose contribution has accelerated in 2015. Internationally reputed insurance and reinsurance leaders often make recourse to alternative capitals. This alternative capacity, whose number of transactions has notably risen, is endowed with various assets. Indeed, it provides a variety of protection sources and better return for investors.

Another advantage, alternative capital comes within the short-term horizon (1-3 years), with hardly any obstacles to entry. According to Guy Carpenter, alternative capital solutions account for 18% of the entire reinsurance offer.

Estimate for total dedicated reinsurance capital

In billions USD Source: AM Best and Guy Carpenter

Source: AM Best and Guy CarpenterIncrease in supply

While alternative capital continues to flow in, traditional reinsurers have also increased their capacity. As of 2010, that is, following the dark years of the subprime crisis, they have gradually consolidated their fundamentals. Because of the absence of major catastrophes and despite the important erosion in the tariffs, from 15% to 20% over recent years, reinsurers have, mostly, posted good results. After an excellent 2014 year, Munich Re reported a net profit of 2.07 billion USD for the first half of 2015. The Munich Group is targeting an annual profit above 3.3 billion USD for 2015 whereas its main objective was ranging between 2.7 and 3.3 billion USD.

Hannover Re, the other global reinsurance giant, is within the same dynamics, generating 590 million USD in net profit by June 30, 2015 and targeting an annual result above its initial forecasts. Based on recent projections, these results should now attain 1.054 billion USD whereas the objective set was of 971 million USD. The French Group, SCOR, on its part, posted 363 million USD in net profit in the first half of the year, that is, a 28% increase over one year. Finally, Swiss Re is expecting results that are consistent with the estimates published in its 2011-2015 plan. The Zurich reinsurer nonetheless reported a net profit amounting to 2.26 billion USD in the first half of 2015, an increase of 11%.

The absence of major catastrophic events

So far, the year 2015 has not witnessed any costly catastrophic events. A downward trend of the intensity of natural catastrophe claims has been noted since 2012, the year when hurricane Sandy struck New York. Combined with the influx of capacity, this milder loss experience has considerably contributed to tariff reduction for non-proportional covers used for this kind of risks.

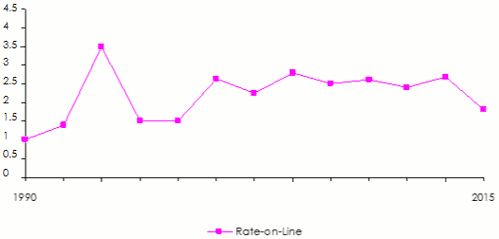

Since hurricane Andrew struck in 1992, the ROL (reinsurer’s premium/reinsurer’s liability), which is the price index used for natural catastrophe business, has been on a steady decline:

Rate-on-Line (in %): natural catastrophes treaties

Source: Guy Carpenter

Source: Guy CarpenterReturn on financial assets at their lowest

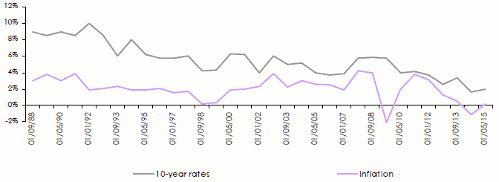

Fighting off inflation has been the priority for most countries endowed with mature economies. Inflation rate has constantly been slipping down since the start of the 1990s and is now located at a record low point. This depreciation has resulted in the reduction of interest rates and the return of financial products in which reinsurers invest. According to Standard & Poor’s, the average return on investment has declined by 30% over the recent four years.

Return on financial products

Sources: Datastream, French market illustrative

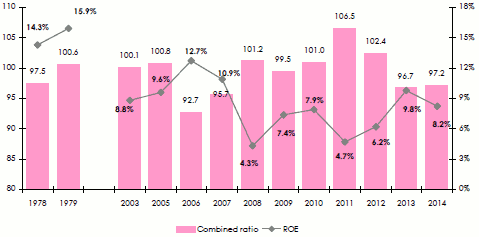

Sources: Datastream, French market illustrativeReinsurers use the return on their investments to set the profitability of their shareholders’ equity. With rate decrease, this strategy becomes difficult to maintain. While in the past it was possible to obtain return on investment of about 15% during the 1970s, the fall of financial products has triggered the decrease in reinsurers’ yields at levels below 10%. This decline in financial revenues has compelled reinsurers to exhibit better technical results, which implies better control of their combined ratio.

Evolution of combined ratio and of return on equity (ROE) 1978-2014

Sources: Overview and Outlook for P&C Insurance industry, May 2015, Swiss Re

Sources: Overview and Outlook for P&C Insurance industry, May 2015, Swiss ReStagnant reinsurance demand

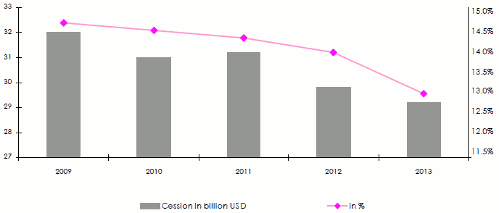

For a long time, capacity needs of ceding companies have been met thanks to traditional reinsurance covers. Yet, this situation is changing. Insurers’ retention is regularly growing thanks to the consolidation of their shareholders’ equity and the improvement of their risk management system. This is particularly true for major insurance groups. The latter have globalized their reinsurance covers not only for the purpose of achieving scale economies, but also in order to seek more sophisticated reinsurance solutions. Hence, the growing boom of alternative reinsurance reported in mature countries.

Evolution of cession rates and premiums ceded by major ceding companies: 2009-2013

Source: SCOR based on annual report data of ACE, Allianz, AIG, AXA, Generali, Zurich

Source: SCOR based on annual report data of ACE, Allianz, AIG, AXA, Generali, ZurichUnderinsurance

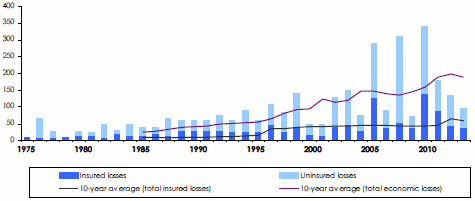

In many countries, insurance penetration rate has progressed less quickly than expected. Underinsurance is partly responsible for that situation. Underinsurance is substantial in the natural catastrophe class of business. During the last ten years, roughly 70% of economic damages caused by major natural events were not insured. This gap between economic losses and insured losses amounts to 1 300 billion USD a year, a situation harnessed by the insurance market which seizes the opportunity to achieve growth, especially in emerging countries such as China, India, Brazil, Indonesia, the Philippines, Thailand and Vietnam.

Evolution of insured and uninsured losses: 1975-2010

Source: Swiss Re Economic Research & Consulting and Cat Perils

Source: Swiss Re Economic Research & Consulting and Cat PerilsCompetition between reinsurers in 2015

With the decrease in reinsurable material, reinsurers are trying to fiercely defend their market shares. Falling rates, rising commissions, the expansion of covers granted have characterized the 2015 renewals for all the classes of business involved. The table below sums up global rate trends noted during the January and July renewals of the ongoing year:

Tariff trends observed during the January and July 2015 renewals: presentation by class of business

| 1st January 2015 | 1st July 2015 | |||||

|---|---|---|---|---|---|---|

| Property reinsurance treaties | ||||||

Australia | 0% to -5% | -5% to -12.5% | ||||

Canada | -10% to -20% | NA | ||||

Central and Eastern Europe | -5% to -20% | NA | ||||

China | -25% to -30% | -15% to -20% | ||||

Europe | -10% to -15% | NA | ||||

France | 0% to -5% | NA | ||||

Germany | 0% to -5% | NA | ||||

Latin America | 0% to -12.5% | 0% to -15% | ||||

MENA region | -5% | -10% | ||||

Nordic countries | -5% to -10% | NA | ||||

Turkey | -10% | NA | ||||

United Kingdom | -15% | -10% | ||||

United States | -10% to -15% | -5% to -20% | ||||

| Excess of loss third party liability treaties | ||||||

Australia | -5% to -10% | -5% to -10% | ||||

Europe (motor third party liability) | -2,5% to -10% | NA | ||||

Europe (other third party liabilities) | -2,5% to -5% | NA | ||||

France | 0% to -3% | NA | ||||

Lloyd’s | -10% to -15% | NA | ||||

United Kingdom (motor third party liability) | 0% to -5% | NA | ||||

United Kingdom (other third party liabilities) | -5% to -20% | NA | ||||

United States (motor third party liability) | -5% to -15% | -5% to -15% | ||||

United States (professional third party liability) | -5% to -15% | -5% to -10% | ||||

United States (other third party liabilities) | ND | -5% to -10% | ||||

| Special risks treaties | ||||||

Aerospace risks | 0% to -7.5% | NA | ||||

Engineering | -15% | NA | ||||

Credit | -20% | NA | ||||

Personal accident and group life insurance | NA | -5% to -20% | ||||

Political risks | NA | -10% | ||||

United States (health) | NA | 0% to 10% | ||||

NA: Not available Source: Willis Re

As previously mentioned, reinsurers are struggling harder and harder in order to satisfy their shareholders with return rates that are consistent with their expectations. With sluggish financial markets, only technical results may still contribute to the provision of profits to investors. A task that has turned out to be increasingly hard to achieve in view of the current context.

It has therefore become essential for reinsurers to carry out a strict selection of portfolio and to diversify reinsurance supply, targeting in particular the coverage of new risks (cyber risks,environmental risks, Solvency II-related reinsurance solutions, etc.).