The digital divide

Called sometimes "digital gap", it rests on the idea that limited access to information and inadequate knowledge or expertise required for ICT (Information Communication Technologies) mastery would trigger irremediable social polarization between individuals and even between regions.

Called sometimes "digital gap", it rests on the idea that limited access to information and inadequate knowledge or expertise required for ICT (Information Communication Technologies) mastery would trigger irremediable social polarization between individuals and even between regions.

In the digital domain, specifically the internet, Africa is lagging behind so much that it had to wait until November 2000 to see the last country, Eritrea, getting connected.

Because of the privatization of the communication sector and the lure of email exchanges with foreign countries, internet has witnesses a rapid growth on the continent despite relatively high prices. The costs pertaining to the establishment of new infrastructure required for the use of the internet network remain exorbitant for many African countries.

The concept of digital divide comprises three main aspects:

- the first one pertains to infrastructure: that is, the possibility or the difficulty of having computers connected to the worldwide network.

- the second relates to training: that is, the ability or the difficulty in using these technologies, which leads to the concept of digital literacy.

- the final aspect is about the use of resources: that is, the factors hindering or those allowing the personal use of the means available on the network.

In Africa, the rapid growth of computer and internet has accelerated the development of several industries, like mobile telephony or more generally telecommunication networks.

Examples of digital divide

The comparison between a few countries may reveal the extent of the gap between nations which are geographically close, but numerically so far apart.

The use of fixed telephony

© Hansueli Krapf, CC BY-SA 3.0 © Hansueli Krapf, CC BY-SA 3.0 |

{kind=link}

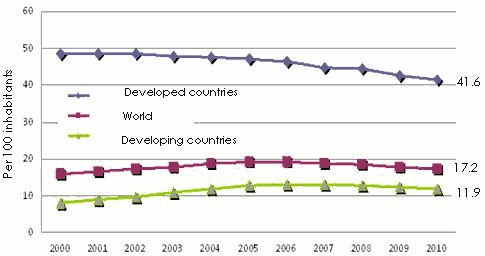

The stationary phone, which is one of the oldest comparative tools in terms of telecommunications, has seen its use decline gradually since the advent of mobile phones.

Between 2006 and 2010, the number of fixed telephone users worldwide has decreased from 1 261 072 071 to 1 188 357 124. The phone is mostly relegated to a strictly professional use or as a means of connecting to the internet.

In 2010, the world record for fixed telephone lines used is of course held by China, with its 294 383 000 lines; that is, 24.77% of all fixed lines listed in the world. China is followed by the United States with 151 171 000 lines, or 12.72% of fixed telephone lines worldwide.

Together, Africa and the Middle East account for only 7.58% of world lines, with 2.56% for Africa and 5.02% for the Middle East.

At the national level, the lowest network coverage rate is reported in the Democratic Republic of Congo, where only 0.06% of the population owns a stationary phone. Topping the list are Canada (50.04%) for America, Switzerland (58.56%) for Europe and Mauritania (29.84%) for Africa.

Fixed telephone lines per 100 inhabitants: 2000-2010

The number of subscriptions to mobile telephony

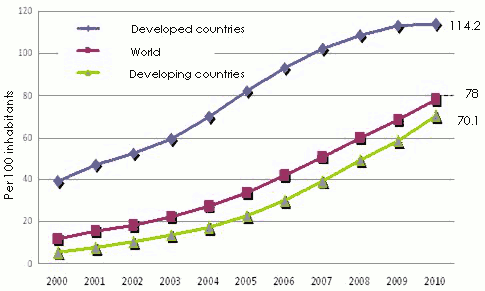

Thanks to the funds devoted to research in developed countries, mobile telephony has become, over the last decade, an extremely innovative and evolving sector.

Thanks to the funds devoted to research in developed countries, mobile telephony has become, over the last decade, an extremely innovative and evolving sector.

In ten years mobile phone subscriptions at the global level have increased more than sevenfold, from 738 193 138 subscribers in 2000 to 5 370 467 196 in 2010.

On the podium of global mobile phone subscriptions, China, unsurprisingly, holds the first position (859 003 000), followed closely by India (752 190 000), and the United States (278 900 000).

Regarding the number of subscribers per capita, Saudi Arabia leads with 1.9 subscriptions per capita. Montenegro with 1.85 subscriptions per capita ranks second while Panama with 1.84 subscriptions per capita comes third.

Subscriptions to mobile telephony per 100 inhabitants: 2000-2010

Despite the very costly telephone equipment and rates, it is in sub-Saharan Africa that we can find the fastest growth over the last five years. For example: Orange hardly charges local calls on French territory, with the bulk of communications being made on unlimited basis. However, one minute call costs 0.10 USD in Tunisia, 0.22 USD in Cameroon or 0.19 USD in Côte d’Ivoire. These variations may seem modest, but compared to minimum wages, one can soon realize the magnitude of the gap.

The internet use

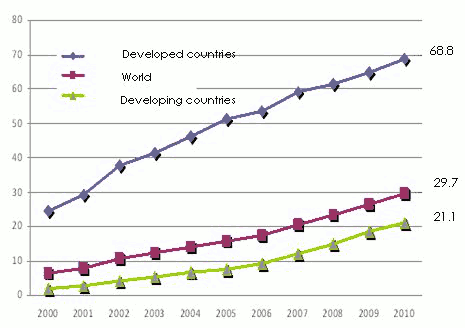

Since the last decade, the use of the internet has increased tenfold in developing countries, going from 2% of the population in 2000 to 21.1% in 2010. These figures remain, nonetheless, below those of the developed countries which posted in 2010 a number of users of 68.8% of the population versus 24.1% in 2000. These different rates do not reflect the reality, though. Developing countries now have more people connected to internet (1 195 000 000 users) than developed countries (849 000 000 users).

The lead taken by developed countries is such that despite the dramatic growth in the number of users in developing countries, the digital divide will still remain in favor of the former.

The lead taken by developed countries is such that despite the dramatic growth in the number of users in developing countries, the digital divide will still remain in favor of the former.

The advantage of the latter is mainly based on the gap between them and the South, first in terms of non-availability of products of equal quality and in terms of price/quality ratio.

Indeed, in most cases, computer equipment in developing countries is outmoded before it gets released in these countries, and not surprisingly so, given that today’s technology is evolving rapidly. Moreover, if a material of equivalent quality is marketed in the South, we will then be facing a population with limited purchasing power. This is true both for the purchase of equipment and for the expenses of internet access, which remains at a low speed but at exorbitant prices.

We must remember that the average price of a computer of acceptable quality today amounts to 500 USD while the minimum wage of a Tunisian citizen is rated at 0.97 USD/h, and that of a Cameroonian at 0.34 USD per hour. Buying a computer would therefore account for 1 470 hours of work for the latter and 515 hours for the former. By analogy, a person living in a developed country earns an average of 9 USD per hour, which means only 55 hours of work are needed to buy a computer.

Percentage of internet users : 2000-2010

Disparities between the prices of computing equipements, connection to the internet network and the minimum wages in certains countries

in USD| Country | Minimum wage/ work hour | Average price of a PC | Nbr of h for the purchase of a PC | Price of internet connection* | Nbr of h of work necessary for an internet connection |

|---|---|---|---|---|---|

France | 11.6 | 500 | 43 | 27 | 2.3 |

Canada | 10.06 | 500 | 50 | 22 | 2.2 |

United States | 6.52 | 500 | 79 | 23 | 3.5 |

Greece | 6.31 | 500 | 79 | 22 | 3.5 |

Saudi Arabia | 4.79 | 500 | 104 | 38.6 | 8 |

Iran | 1.81 | 500 | 276 | 187.6 | 104 |

Tunisia | 0.97 | 500 | 515 | 16.47 | 17 |

Cameroon | 0.34 | 388 | 1470 | 148 | 435 |

Special cases of Africa and the Middle East

The Middle East

While the standard of living of the vast majority of the Middle East population is high, it is surprising to notice that the number of internet users is limited to only 3.3% of the total number of these same users. The growth rate of the network is 1987% for the period from 2000 to 2011. By June 30, 2011, the rate of internet penetration is of 33.5% or 72 497 466 persons connected to the network on a total of 216 258 843 living in this region.

Number of internet user per country in the Middle East

| Population 2011* | Users in December 2000 | Users in June 2011 | Penetration in % | Users in % | |

|---|---|---|---|---|---|

Bahrain | 1 214 705 | 40 000 | 649 300 | 53.5 % | 0.9 % |

Iran | 77 891 220 | 250 000 | 36 500 000 | 46.9 % | 50.3 % |

Iraq | 30 399 572 | 12 500 | 860 400 | 2.8 % | 1.2 % |

Israel | 7 473 052 | 1 270 000 | 5 263 146 | 70.4 % | 7.3 % |

Jordan | 6 508 271 | 127 300 | 1 741 900 | 26.8 % | 2.4 % |

Kuwait | 2 595 628 | 150 000 | 1 100 000 | 42.4 % | 1.5 % |

Lebanon | 4 143 101 | 300 000 | 1 201 820 | 29.0 % | 1.7 % |

Oman | 3 027 959 | 90 000 | 1 465 000 | 48.4 % | 2.0 % |

Palestine | 2 568 555 | 35 000 | 1 379 000 | 53.7 % | 1.9 % |

Qatar | 848 016 | 30 000 | 563 800 | 66.5 % | 0.8 % |

Saudi Arabia | 26 131 703 | 200 000 | 11 400 000 | 43.6 % | 15.7 % |

Syria | 22 517 750 | 30 000 | 4 469 000 | 19.8 % | 6.2 % |

United Arab Emirates | 5 148 664 | 735 000 | 3 555 100 | 69.0 % | 4.9 % |

Yemen | 24 133 492 | 15 000 | 2 349 000 | 9.7 % | 3.2 % |

") Even though some countries like Qatar, Palestine, Bahrain and the United Arab Emirates exhibit penetration rates above 50%, the average rate of this region remains relatively low (33.7%). Connection speed is slow sometimes for relatively high subscription rates.

Even though some countries like Qatar, Palestine, Bahrain and the United Arab Emirates exhibit penetration rates above 50%, the average rate of this region remains relatively low (33.7%). Connection speed is slow sometimes for relatively high subscription rates.

A major reason for the slow development of broadband in the Middle East is the small amount of Arabic content on the web. The language disadvantage is such that users do not see the value of having a faster connection than the one they need for the limited daily use.

Africa

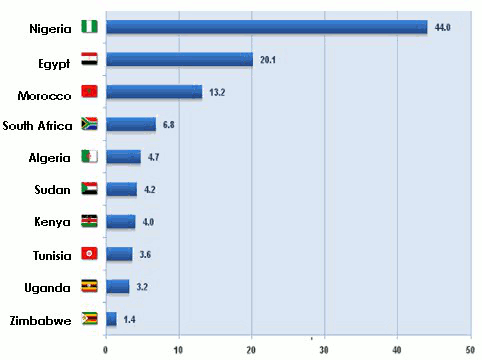

Globally, Africa is by far the last in terms of internet use. With barely 118 609 620 people connected for a population of 1 037 524 058 people, Africa has a penetration rate of 11.4%, accounting only for 5.7% of the number of users connected to the internet.

Population and internet users*

| Population 2011** | World population in % | Internet users | Penetration in % | Use growth (2000-2011) | Users in % | |

|---|---|---|---|---|---|---|

Africa | 1 037 524 058 | 15% | 118 609 620 | 11.4 % | 2 527.4 % | 5.7% |

Rest of the world | 5 892 531 096 | 85% | 1 976 396 385 | 33.5 % | 454.4 % | 94.3% |

Total | 6 930 055 154 | 100% | 2 095 006 005 | 30.2 % | 480.4 % | 100% |

The 10 countries having the most internet users at 31 March 2011 (in millions of users)

Paradoxically, it is indeed Africa which, in terms of number of users connected over the past decade, reports the highest growth rate: 2527% versus 454.4% for the rest of the world and 480% of overall average for the whole world during the same period.

Africa is evolving from a situation of scarcity to that of overcapacity. It is therefore wise to assume that it has a promising future with regard to reducing the digital divide that separates it from developed countries. Unfortunately this growth is mainly for about ten countries which are leading the race on the continent. With the number of users lacking quality, African countries are still far from being competitive to withstand rival developed countries.

Africa is evolving from a situation of scarcity to that of overcapacity. It is therefore wise to assume that it has a promising future with regard to reducing the digital divide that separates it from developed countries. Unfortunately this growth is mainly for about ten countries which are leading the race on the continent. With the number of users lacking quality, African countries are still far from being competitive to withstand rival developed countries.

The main reasons for the growth of digital technology in Africa can be summarized as follows:

- a promising population dynamics, resulting in a young population receptive to new technologies.

- a sustained economic growth in recent years for most of the continent, enhancing the purchasing power of a rising middle class.

- a greater governmental involvement in the definition of master plans related to new technologies.

It is important to note that the development of internet in Africa takes place primarily through the development of mobile internet. This formula is proposed at more attractive prices well in keeping with the income and purchasing power of different social classes. According to one estimate of the International Telecommunication Union (ITU), the number of mobile internet subscribers increased from 7 million 3 years ago to 29 million today.

In addition, during the last decade, many development projects for the African network have been completed. Others are planned, especially those pertaining to the installation of submarine cables linking the main coasts of Africa to European countries.

The major projects underway on the west coast are named: WACS, ACE and SAex.

The WACS project (West Africa Cable System) has been initiated by MTN, Telkom and Vodacom. This is a 14 000 km long submarine cable in fiber optics which links London to South Africa along the West African coast. The cable is already installed and should be operational by mid 2012. With a capacity of 5.120 Tb/s, it will increase the capacity of African connections by 23%.

The ACE project (Africa Coast to Europe) is the work of a consortium led by France Télécom. This 17 000 km long cable will connect France to South Africa via Spain. Its construction cost is estimated at 700 million USD. It should ultimately provide a total capacity of 5.120 Tb/s and connect 23 African countries during the first half of 2012.

The SAex project (South Atlantic Express) will link South Africa and Angola to Brazil. With a length of 10 000 km, SAex will cost 375 million USD, and will be operational before June 2013.