Founded in 2016, CCR Re began its commercial reinsurance activities as a subsidiary of Caisse Centrale de Réassurance (CCR), a state-owned entity entrusted with natural catastrophe risks and the management of public funds.

In 2023, the company was privatized, with 75% of its capital sold to two partners from the mutual insurance sector, Société Mutuelle d'Assurance du Bâtiment et des Travaux Publics (SMABTP) and Mutuelle Assurance du Corps Sanitaire Français (MACSF).

Based in Paris, CCR Re is currently France's second-largest reinsurer.

By 31-12-2023, CCR Re is

- a life and non-life reinsurer

- a head office in Paris

- a share capital of 109 million EUR (120 million USD)

- a shareholders' equity worth 776 million EUR (856 million USD)

- assets worth 4.175 billion EUR (4.608 billion USD)

- a turnover of 1.186 billion EUR (1.309 billion USD)

- a net income of 56 million EUR (62 million USD)

- a combined non-life ratio of 96.6%

- a 2.4% return on invested assets

- a solvency ratio of 208%

- ROE of 7.2%

- ratings: A / stable (AM Best) and A / stable (S&P)

- a network comprising a representative office in Lebanon and two branches in Canada and Malaysia

- a market encompassing 80 countries

- 176 employees

CCR Re: historical background

The history of CCR Re is closely linked to that of Caisse Centrale de Réassurance (CCR), a historic player in the French market, whose establishment dates back to the aftermath of the Second World War. In France, the 1945-1946 period was marked by government interventionism affecting the financial sector, with the nationalization of 34 insurance companies, accounting for around 50% of premium income in 1945.

In April 1946, the then provisional government created the CCR under the same legislation nationalizing direct insurance companies.

April 1946, set up by the authorities, the CCR, a separate entity from the French insurance market, was tasked, with the guarantee of the State, with:

- managing the compulsory legal cession of 4% ceded by all direct insurers,

- developing certain risks of economic and social interest to France,

- managing certain State guarantees,

- developing market reinsurance activities.

1969, CCR contributes to the establishment of Société Commerciale de Réassurance (SCOR), in which it held a 48.1% stake. The entire market reinsurance portfolio is transferred to the new entity. CCR's stake in SCOR is subsequently sold.

1979, CCR obtains authorization from the supervisory ministry to practice commercial reinsurance with no State guarantee.

1982, following the enactment of the French Natural Catastrophe Act, CCR set up reinsurance coverage with a government guarantee. The aim of this solution was to support French insurance companies and reduce the lack of protection against certain cumulative risks that could lead to the bankruptcy of a direct market player.

The law covers all risks of an exceptional nature, including natural disasters, war risks, nuclear risks, terrorist attacks and acts of terrorism.

1987, CCR was authorized to relaunch its market reinsurance activities, provided that these did not exceed one-third of its total turnover, a solution that had lingered on until 2016, when CCR Re was established.

1992, CCR changed its legal status, abandoning its status as a public industrial and commercial establishment and becoming a limited company.

2016, CCR separates its reinsurance activities for exceptional risks from its market activities, transferring its commercial portfolio to its newly-created subsidiary CCR Re.

2017, CCR Re officially begins operations. With a starting share capital of 90 million EUR (95 million USD), CCR Re officially begins operations on 1 January 2017.

Following the demerger, CCR retains its two main mandates, namely state-guaranteed activities and the management of public funds on behalf of the State, such as the National Guaranty Fund for Agricultural Disasters (FNGRA) and the Compensation Fund for Construction Insurance Risks (FCAC).

2023, CCR sells 75% of its subsidiary CCR Re to the SMABTP and MACSF groups. CCR retains only 24.82% of CCR Re's capital.

|  |

Bertrand Labilloy Chief Executive Officer | Laurent Montador Deputy Chief Executive Officer |

1945

Nationalization of 34 insurance companies in FranceApril 1946:

Establishment of Caisse Centrale de Réassurance (CCR)1969

Establishment of Société Commerciale de Réassurance (SCOR)1979

CCR authorized to practice commercial reinsurance with no State guarantee1982

CCR set up reinsurance coverage with State guarantee1987

CCR authorized to relaunch its market reinsurance activities1992

Change in CCR's legal status2016

Establishment of CCR Re, a CCR subsidiary2017

CCR Re officially begins operations2023

Change in CCR Re's shareholder structure, with 75% of the capital sold to the SMABTP and MACSF groups

CCR Re, from the start to the present day

The life and non-life reinsurance license issued to CCR Re by the supervisory authorities was published in the Official Gazette on 10 November 2016.

The company effectively started operations on 1 January 2017, with significant advantages, including a portfolio inherited from the parent company, of 443 million EUR (467 million USD), shareholders' equity in the order of 760 million EUR (801 million USD), qualified staff and access to over 60 markets spread over several continents.

In addition, AM Best and Standard & Poor's have awarded CCR Re ratings of A and A- respectively, with a stable outlook.

Despite these strengths, CCR Re ended the 2017 year with a lower turnover in its original currency, dwindling from 443 million EUR (467 million USD) in 2016 to 396 million EUR (474 million USD) (1) a year later. This decline is due to a more cautious underwriting policy than the one pursued in the past, and net business terminations in Northern Europe.

(1) Expressed in dollars, 2017 turnover (474 million USD) were up compared to those expressed in the same currency in 2016 (467 million USD). This difference between premium growth rates in the two currencies is due to the sharp devaluation of the EUR in 2017, from 1 EUR= 1.05353 USD in 2016 to 1 EUR= 1.19786 USD in 2017

The privatization

In July 2023, seven years after its inception, CCR Re was privatized. The consortium made up of the SMABTP group, specialized in construction risks, and MACSF, expert in medical risks, took over 75% of the capital, with CCR maintaining around 25%.

The transaction price before the capital increase amounted to 947 million EUR. In the end, CCR Re is valued at 968 million EUR after CCR has sold its IT system.

The effects of this privatization are immediate. Indeed, share capital, which has remained constant since the company's establishment, rose from 90 million EUR (96 million USD) at the end of 2022 to 109 million EUR (120 million USD) at the end of 2023, an increase of 21%. Shareholders' equity, which has been rising steadily since 2016, jumped by 44.5% in a single year, from 537 million EUR (573 million USD) in 2022 to 776 million EUR (856 million USD) in 2023.

Assets are on the same upward curve, rising by 15.5% in 2023 to 4.175 billion EUR (4.608 billion USD).

This new financial base will enable CCR Re to:

- strengthen its underwriting capabilities,

- have the means to realize its business plan,

- retain the confidence of its shareholders,

- comply with the Solvency 2 framework and standards,

- achieve synergies in information, IT and risk management systems,

- have a solid rating: A from S&P and A from AM Best with stable outlook.

Evolution of capital, shareholders' equity and assets: 2016-2023

Figures in millions

| Share capital | Shareholders’ equity | Total assets | ||||

| EUR | USD | EUR | USD | EUR | USD | |

| 2023 | 109 | 120 | 776 | 856 | 4 175 | 4 608 |

| 2022 | 90 | 96 | 537 | 573 | 3 615 | 3 859 |

| 2021 | 90 | 102 | 507 | 574 | 3 228 | 3 655 |

| 2020 | 90 | 111 | 472 | 580 | 2 944 | 3 616 |

| 2019 | 90 | 101 | 453 | 507 | 2 507 | 2 807 |

| 2018 | 90 | 103 | 418 | 478 | 2 329 | 2 664 |

| 2017 | 90 | 108 | 384 | 460 | 2 209 | 2 646 |

| 2016 | 90 | 95 | 367 | 387 | 2 212 | 2 330 |

CCR Re goes international

CCR Re underwrites treaties in 80 countries. Its diversified portfolio includes ceding companies of all sizes.

|

Pierre Salameh Director of Lebanon Representative Office - P&C |

The company, which avoids underwriting in areas overexposed to natural catastrophes (United States, Australia, New Zealand, etc.), is focusing its development on regions with high growth potential, such as Latin America, for both life and non-life business, Africa and Asia.

The company has three offices abroad:

- a branch in Canada, "CCR Re Canada",

- a representative office in Lebanon, tasked with non-life business in the MENA zone. This office has been active for over 25 years,

- a branch in Labuan, Malaysia.

According to Laurent Montador, Deputy Chief Executive Officer, CCR Re has no immediate plans to develop new locations. From its technical base in Paris, it favors a centralized underwriting model, with intensive travel by its teams in the field.

CCR Re: Shareholding

Since 3 July 2023, when the SMABTP and MACSF consortium acquired a stake in CCR Re, the reinsurer's shareholder structure has been as follows:

| Shareholders | In % |

| SMABTP | 47.93% |

| SMA Vie BTP | 8.46% |

| CCR | 24.82% |

| MACSF Assurances | 13.78% |

| MACSF ER | 5.01% |

CCR Re: Management

| Patrick Bernasconi | Chairman of the Board of Directors |

| Bertrand Labilloy | Chief Executive Officer (CEO) |

| Laurent Montador | Deputy CEO |

| Isabelle Bion | Chief Financial Officer (CFO) |

| Sylvie Chanh | Chief Legal, Claims and Services Officer |

| Mathieu Halm | Chief Retrocession & Alternative Capital Officer and Board Secretary |

| Jérôme Isenbart | Chief Risk Officer and Actuary |

| Hind Mechbal | Chief Information Officer |

| Hervé Nessi | Chief Underwriting Officer |

| Marlène Larsonneur | Chief Human Resources Officer, Communication and Facilities |

CCR Re, a young and multicultural team

CCR Re : The portfolio

The smooth transfer of the CCR portfolio to CCR Re not only enabled the new entity to assume underwriting continuity, but also made it easier to maintain long-established relationships with ceding companies.

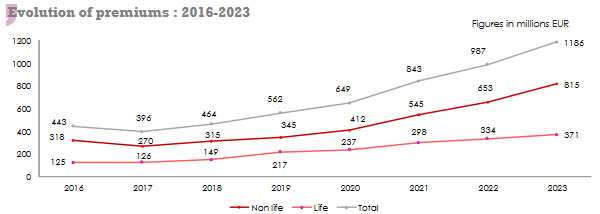

After 2017, a year of transition, the constantly growing portfolio passed the symbolic 1 billion EUR mark at the end of 2023, closing the year at 1.186 billion EUR (1.309 billion USD).

This turnover growth of almost 200% from 2017 to 2023 is all the more remarkable given that it was achieved in extremely difficult market conditions: Covid-19 pandemic, inflation and rising natural catastrophe claims.

At the end of 2023, the portfolio was dominated by the non-life segment, which accounted for 69% of underwritings, having grown by 202% over the 2017-2023 period. The strong non-life performance is mainly due to underwritings in Canada and Latin America.

The life business, which has grown by 194% over the past seven years, recorded 11% growth in 2023.

Underpinned by good solvency, this growth in life and non-life business reflects CCR Re's strong financial and operational momentum.

Life and non-life premiums

Figures in millions

| Life | Non-life | Total | ||||

| EUR | USD | EUR | USD | EUR | USD | |

| 2023 | 371 | 409 | 815 | 900 | 1 186 | 1 309 |

| 2022 | 334 | 357 | 653 | 697 | 987 | 1054 |

| 2021 | 298 | 337 | 545 | 617 | 843 | 954 |

| 2020 | 237 | 291 | 412 | 506 | 649 | 797 |

| 2019 | 217 | 243 | 345 | 386 | 562 | 629 |

| 2018 | 149 | 170 | 315 | 360 | 464 | 530 |

| 2017 | 126 | 151 | 270 | 323 | 396 | 474 |

| 2016 | 125 | 132 | 318 | 335 | 443 | 467 |

| 2017-2023 evolution | 194% | 171% | 202% | 178% | 199% | 176% |

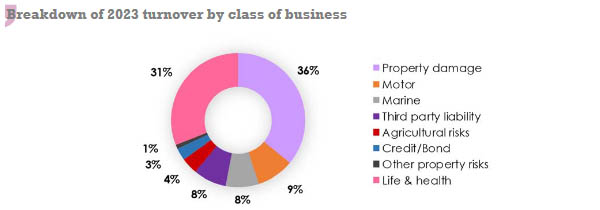

Premiums by class of business: 2016-2023

The non-life insurance is driven by that of property, with 36% of premiums written, followed by motor (9%), with transport and third-party liability each accounting for 8%. Life and health insurance, meanwhile, mainly comprises provident (28%) and health (7%) products.

Figures in millions USD

| 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2023 shares | |

| Property damage | 112 | 118 | 138 | 170 | 222 | 290 | 342 | 477 | 36% |

| Motor | 65 | 53 | 69 | 69 | 107 | 105 | 105 | 117 | 9% |

| Marine | 28 | 29 | 26 | 26 | 60 | 68 | 83 | 108 | 8% |

| Third party liability | 27 | 19 | 22 | 19 | - | 68 | 77 | 99 | 8% |

| Agricultural risks | 14 | 24 | 26 | 19 | 31 | 31 | 35 | 45 | 4% |

| Credit/Bond | 33 | 24 | 21 | 26 | 26 | 30 | 35 | 35 | 3% |

| Other property risks | 56 | 56 | 58 | 57 | 60 | 25 | 20 | 18 | 1% |

| Non-life total | 335 | 323 | 360 | 386 | 506 | 617 | 697 | 899 | 69% |

| Life and disability | 108 | 123 | 116 | 169 | 189 | 226 | 250 | 278 | 21% |

| Health | 24 | 28 | 38 | 51 | 68 | 74 | 68 | 86 | 7% |

| Long-term care | - | - | 10 | 12 | 23 | 24 | 25 | 24 | 2% |

| Other life risks | - | - | 6 | 11 | 11 | 13 | 14 | 21 | 1% |

| Life and health total | 132 | 151 | 170 | 243 | 291 | 337 | 357 | 409 | 31% |

| Grand total | 467 | 474 | 531 | 629 | 797 | 955 | 1054 | 1309 | 100% |

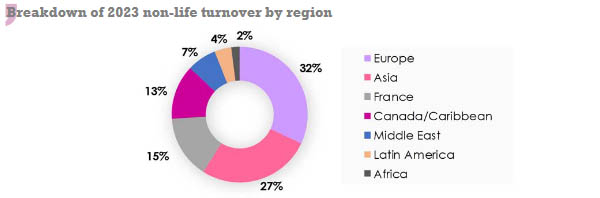

Premiums by region: 2020- 2023

Non-life insurance

The breakdown of non-life turnover by geographic region highlights the weight of Europe, which accounts for 47% of the portfolio, including 15% for the French market alone. Asia comes second with 27% of underwritings.

The Canada-Caribbean, Middle East, Latin America and Africa zones follow in descending order, with market shares of 13%, 7%, 4% and 2% respectively.

Figures in millions

| 2020 | 2021 | 2022 | 2023 | Parts 2023 | |||||

| EUR | USD | EUR | USD | EUR | USD | EUR | USD | ||

| Europe | 210 | 258 | 267 | 302 | 320 | 341 | 383 | 422 | 47% |

| * including France | 115 | 141 | 87 | 98 | 111 | 118 | 122 | 134 | 15% |

| Asia | 107 | 131 | 142 | 161 | 176 | 188 | 220 | 243 | 27% |

| Canada Caribbean | 70 | 86 | 65 | 74 | 72 | 77 | 106 | 117 | 13% |

| Middle East | 25 | 31 | 44 | 50 | 52 | 56 | 57 | 63 | 7% |

| Latin America | - | - | 16 | 18 | 13 | 14 | 33 | 36 | 4% |

| Africa | - | - | 11 | 12 | 20 | 21 | 16 | 18 | 2% |

| Non-life total | 412 | 506 | 545 | 617 | 653 | 697 | 815 | 899 | 100% |

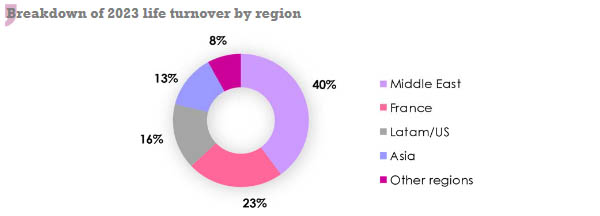

Life & health insurance business by region: 2020-2023

The life and health insurance portfolio is particularly strong in the Middle East, which accounts for 40% of turnover. France, the Americas and Asia follow with shares of 23%, 16% and 13% respectively.

Figures in millions

| 2020 | 2021 | 2022 | 2023 | 2023 shares | |||||

| EUR | USD | EUR | USD | EUR | USD | EUR | USD | ||

| Middle East | 95 | 117 | 116 | 132 | 124 | 132 | 149 | 164 | 40% |

| France | 71 | 87 | 77 | 87 | 93 | 99 | 85 | 94 | 23% |

| Latam/US | 16 | 20 | 24 | 27 | 37 | 40 | 59 | 65 | 16% |

| Asia | 43 | 53 | 63 | 71 | 53 | 57 | 48 | 53 | 13% |

| Other regions | 12 | 14 | 18 | 20 | 27 | 29 | 30 | 33 | 8% |

| Life total | 237 | 291 | 298 | 337 | 334 | 357 | 371 | 409 | 100% |

CCR Re : Technical ratios and net result (2016-2023)

The loss ratio for the year ending 31 December 2023 is set at 67.3%, down 1.8 points on 2022. Natural catastrophes in 2023 penalized CCR Re as it lost 13 points. With a net cost of 62.1 million EUR (91.3 million EUR gross of retrocession), these natural catastrophe claims pertain in particular to hail in Italy, earthquake in Turkey, hurricane Otis in Mexico, storm Ciaran in France and typhoon Doksuri in Asia.

The combined ratio for 2023 amounts to 96.6%, an improvement of 2.1 points on 2022. Thanks to tight control of non-life management costs, which have been falling steadily for the past three years, the combined ratio for 2023, along with that for 2021 (also 96.6%), is the lowest recorded since CCR Re was founded.

It is worth noting that the 2020 year, heavily impacted by the explosion in the port of Beirut on 4 August 2020 and by Covid-19 claims, sustained a loss ratio of 73.7%, down 7.1 points on 2019, and a combined ratio of 103.2%, up 5.1 points on the previous year.

In another notable development, the sharp inflation that set in during 2022 weighed on the accounts of insurers and reinsurers. Global inflation rates, which rose sharply from 1.9% in 2020 to 3.4% in 2021 and peaked at 8% in August 2022 (1), increased the 2022 loss experience of all market players. CCR Re has not been immune to this deterioration, recording a 2.6% increase in its claims cost, from 66.5% in 2021 to 69.1% in 2022.

(1) World Bank

Evolution of ratios (2016-2023)

| 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | |

| Net loss ratio | 75.10% | 73.90% | 68.00% | 66.60% | 73.70% | 66.50% | 69.10% | 67.30% |

| Net management expenses ratio | 31.60% | 31.00% | 31.40% | 31.50% | 29.50% | 30.10% | 29.60% | 29.30% |

| Net combined ratio | 106.70% | 104.90% | 99.40% | 98.10% | 103.20% | 96.60% | 98.70% | 96.60% |

Net result

With 56 million EUR (62 million USD) realized in 2023, or 4.72% of written premiums and a return on equity of 7.2%, CCR Re has achieved, in monetary terms, the best net result since its creation. This 33% jump in net income in 2023 is supported by strong growth in underwriting results, up by 63% year-on-year (62 million EUR in 2023 vs. 38 million EUR in 2022).

Figures in millions

| Net investment income | Net technical result | Net result | ||||

| EUR | USD | EUR | USD | EUR | USD | |

| 2023 | ND | ND | 62 | 68 | 56 | 62 |

| 2022 | 47 | 50 | 38 | 41 | 42 | 45 |

| 2021 | 36 | 41 | 48 | 54 | 41 | 46 |

| 2020 | 47 | 58 | 19 | 23 | 18 | 22 |

| 2019 | 49 | 55 | 47 | 53 | 35 | 39 |

| 2018 | 43 | 49 | 26 | 30 | 35 | 40 |

| 2017 | 38 | 46 | 16 | 19 | 17 | 20 |

| 2016 | 32 | 34 | 15 | 16 | 6 | 6 |

NA : not available

CCR Re: Strategy and positioning

Well-resourced since its inception, CCR Re has succeeded in building on the heritage handed down by its parent company. The company has proven resilient during the Covid years, developing a balanced portfolio with steadily improving results.

Positioning

After the successful phases of establishment and result consolidation, the new shareholders find themselves well-positioned to build a portfolio that meets their expectations and would make CCR Re a major player on the French market.

On the basis of solid fundamentals and green technical and financial indicators, the company has, in the words of its management, every opportunity to devise a strategy based on:

- maintaining good business relationships with ceding companies,

- selective underwriting, excluding risks located in the United States (natural catastrophes,…),

- a cautious provisioning policy,

- prompt claims settlement,

- a high-quality service offering,

- the implementation of a retrocession program offering optimal protection,

- the establishment of synergies between the various business units,

- a young, multicultural team,

- multiline underwriting in traditional property, health, life and liability classes of business, coupled with specialty risks (aviation, space, marine, credit & bond,…),

- the integration of environmental, social and governance (ESG) criteria into reinsurance and investment activities.

Transformation and innovation

In order to keep up with the digital transformation that Covid has accelerated, CCR Re, like many other players, is turning to new technologies and innovation. A review of processes has already been carried out, so as to gradually integrate artificial intelligence into many areas of activity, such as underwriting, actuarial analysis, accounting and support functions. These include:

- the overhaul of the life group quoting portal, scheduled for launch in 2024,

- the implementation of a data platform with the aim of centralizing data,

- the development of pricing tools for substandard risks,

- the use of new technologies and innovative decision-making tools,

- the creation of targeted internal working tools,

- the adoption of generative artificial intelligence and data mining,

- the automation of certain services such as reporting.

Forecasts and objectives

Every new reinsurance company has a number of objectives: to achieve critical mass, to meet technical and solvency criteria, to obtain and/or maintain a good rating, and to meet shareholder expectations. CCR Re is no exception to these imperatives. Still, according to its Deputy CEO Laurent Montador, by 2027, the company aims to:

- become a benchmark player on the Paris marketplace,

- improve its position against the major reinsurers,

- develop an approach based on personalized service,

- double the turnover to 2 billion EUR,

- maintain adequate solvency,

- improve profitability by 300 basis points,

- achieve a combined ratio of between 92% and 94%,

- guarantee a double-digit return on equity (ROE).

Like the insurer, the reinsurer is not only subject to a technical risk that impacts the liabilities side of its balance sheet, but also to the threat of a financial risk that deteriorates the quality of the assets representing its commitments.

To protect its balance sheet, the insurance and reinsurance company has no other solution than technical rigor, to mitigate the claims generated by accumulations and peak risks, and securing its investments, to protect itself from the volatility of the financial markets.

Other challenges, which appear to be just as important as those mentioned above, involve maintaining autonomy of action, improving the internal control system, automating compliance processing and improving digitized processes.

CCR Re can only achieve these objectives with a diversified and balanced portfolio that meets the technical and financial standards of the profession.

| Exchange rate * | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 |

| 1 EUR/USD | 1.05356 | 1.19786 | 1.14379 | 1.11986 | 1.22824 | 1.1324 | 1.06749 | 1.10364 |

* as at 31/12