International tensions, economic slowdown, and debt are weakening companies and increasing the risk of default. It is in this unfavorable operating environment that the credit insurance market is currently evolving.

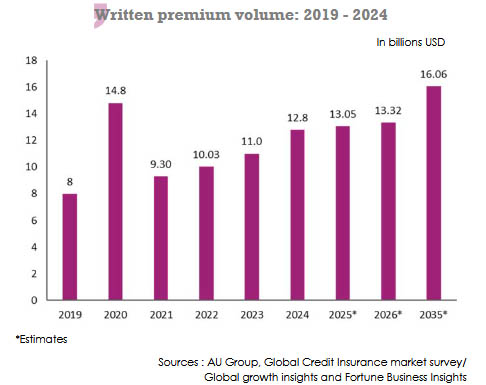

In 2024, the credit sector generated 12.8 billion USD in premiums. Back then, its combined ratio stood at 76%, below the average of 80% recorded over the past ten years. This performance can be explained by strict underwriting discipline and selective support for policyholders.

The credit insurance market even managed to withstand the Covid-19 crisis which put a significant number of companies under severe strain. It should be noted that in 2020, premiums in the sector soared to 14.8 billion USD. The economic shock caused by the Covid-19 health crisis led to a massive underwriting wave by economic operators to guard against the risk of default.

Thanks to government bailout plans and low claims rates, demand for coverage declined in 2021 and premiums returned to their pre-crisis level of between 8 and 9 billion USD.

The market has ever since evolved in an increasingly competitive environment, compounded by the arrival of new players: financial institutions, MGAs (Managing General Agents) and CDS (Credit Default Swap) providers.

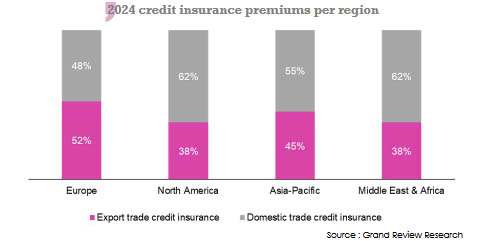

Credit insurance market: regional structure

The credit insurance market features significant geographical disparities resulting from the specific economic situation in each region, the level of trade, and the regulatory frameworks in force.

Below, we present the credit insurance market in the four main regions: North America, Europe, Asia-Pacific, and Africa/Middle East.

North America dominates the global credit insurance market with 4.3 billion USD in premiums written in 2024 and a market share of 31%. The stability of the economic environment and the maturity of financial infrastructures favor a high penetration rate for this line of business, a momentum that rests on:

- integration of credit insurance solutions (Factoring/Supply Chain Finance/Securitization) within the banking network,

- a dense network of brokers,

- sustained underwriting of medium and large companies.

The United States is at the forefront of the American market, with estimated revenues of 3.73 billion USD in 2025, driven mainly by rising default risks.

Europe is a mature and well-structured market. In 2024, credit insurance premiums were estimated at 3.54 billion USD and are expected to reach 3.84 billion USD in 2025. Underwriting is expected to grow at an average annual rate of 8%, driven mainly by the increase in the risk of corporate bankruptcy.

Geopolitical tensions, growing liquidity protection needs, cross-border transactions, new technologies, and government initiatives are also supporting this growth.

The United Kingdom, Germany, and France are among the main drivers of the European credit market.

The Asia-Pacific region is experiencing rapid growth in this sector, an expansion is driven by regional economic growth, the gradual adoption of credit by SMEs, and the resurgence of corporate insolvency risk.

The size of the Asian market was estimated at 2.82 billion USD by the end of 2024. China and India are the main contributors to this growth, with premiums estimated at 700 million USD and 610 million USD respectively in 2024(2).

The Middle East and Africa regions are showing steady growth, driven by economic diversification policies, the expansion of international trade, and growing demand for risk management solutions.

The total volume of premiums written in the region is estimated at nearly 1 billion USD, with the Gulf Cooperation Council States alone accounting for nearly 50% of this amount.

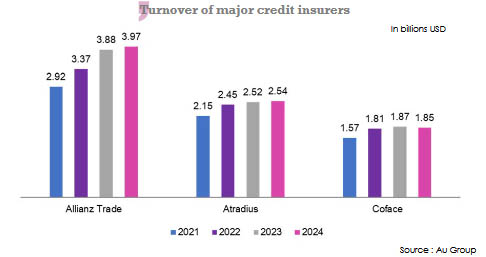

Credit insurance: market players

The credit market is highly concentrated, with three major players, namely Allianz Trade (formerly Euler Hermes), Atradius, and Coface, accounting for 65% of total global premiums in 2024.

This oligopolistic dominance is a result of the specific characteristics of credit insurance. Indeed, this activity requires specialized expertise in risk analysis, a strong financial base, and an extensive international network.

These barriers to entry eliminate many potential insurers. As a result, only a few specialized companies manage to serve a diverse clientele consisting of exporters, multinationals, and companies integrated into global supply chains.

In addition to credit risk coverage, these players have gradually diversified their activities by offering related services such as:

- Allianz Tradewhich offers fraud prevention solutions and bond insurance.

- Atradius which offers credit and bond reinsurance products through its subsidiary Atradius Re.

- Coface which focuses on factoring and debt collection.

Allianz Trade

With a market share of 31% in 2024, Allianz Trade is the world leader in credit insurance. The insurer benefits from the strategic support and international network of its parent company, Allianz Group, one of the world's leading insurers, with a physical presence in more than 70 countries.

Building on the expertise developed by Euler Hermes, founded in 1918, Allianz Trade, headquartered in Paris, supports companies in securing their trade receivables. The insurer also offers solutions tailored to large infrastructure and energy projects.

Atradius

Atradius is the world's second-largest credit insurer. Based in Amsterdam (Netherlands) and operational in more than 50 countries, the company offers a comprehensive range of credit insurance, bond, debt collection, and reinsurance solutions tailored to corporate needs.

Its international presence and specialization in foreign trade make Atradius a key player in securing commercial transactions.

Coface

Ranking as the third largest player worldwide, the French Foreign Trade Insurance Company (Coface) stands out for its long-lasting commitment to supporting exporters and its expertise in emerging markets.

In 2024, the group posted a turnover of 1.85 billion USD and net income of 272 million USD, up 8.6% from the previous year. With more than 5 200 employees in around 100 countries and a portfolio of over 100 000 clients, Coface holds a strategic position in securing trade, particularly between Europe and Africa.

The geographical distribution of its turnover reflects this diversification: 29.2% of premiums come from the Mediterranean and Africa, 21.2% from Western Europe, 19.6% from Northern Europe, and 9.6% from North America.

This balanced presence enables Coface to play a facilitating role in trade relations between different continents.

These three global leaders are joined by other renowned players, notably insurers AIG (United States), QBE (Australia), Chubb (United States), and Credendo (Belgium). Banking institutions are also active in the credit segment.

However, the complexity of risk analysis and the need for extensive databases on corporate creditworthiness give the three long-standing players a lasting competitive advantage.

To complete the picture, it is worth noting that many public entities offer credit guarantees, often focusing on their local market and/or specific niches. This is the case, for example, with Sinosure (China Export & Credit Insurance Corporation), a Chinese company founded in 2001, the only export credit insurer in China. Among other things, it supports the national policy of promoting foreign trade.