As an alternative to conventional insurance, takaful is currently booming in countries that have introduced Islamic finance.

Backed by the enactment of specific regulatory frameworks, the market is focusing its development on the establishment of new takaful or window companies, and on mergers between players already operating in the sector. The introduction of new technologies within companies is helping to upgrade their structures and working methods.

With the consolidation of the market and the modernization of structures, takaful insurance can only improve its financial performance.

Growth in the number of takaful insurance companies

By 2022, the global market accounted for 344 companies dedicated exclusively to Takaful and Retakaful.

These companies operate in over sixty-five countries, mainly in the MENA and South-East Asia zones. In 2012, the market counted just 274 operators of this type, that is an increase of 25% in a decade.

Takaful insurance market: key indicators

A relatively new business, takaful insurance, which by the end of 2023 generated a turnover of almost 34 billion USD, offers promising growth prospects.

Significantly improved underwriting results, achieved through prudent risk management, bear witness to the steady improvement in the performance of this insurance business.

According to the Islamic Development Bank Group, 77% of takaful operators were profitable in 2022. Contributions or premiums collected have grown steadily over the past ten years, mainly in the motor and family (life) lines.

This growth is driven by:

- the solid financial performances achieved by the main market players,

- the increase in the number of players operating in the market, with the number of takaful companies having risen from 274 in 2012, to 344 in 2022,

- transparency of operations and good communication of market data,

- a better legislative framework with the promulgation of a specific regulatory framework in many countries,

- increased policyholder awareness of the need for life and health protection to mitigate rising healthcare costs,

- improved compliance with capital requirements,

- the introduction of new takaful products to meet customer needs,

- consolidation of the takaful insurance market through mergers and acquisitions particularly in Saudi Arabia and the United Arab Emirates,

- the development of 100% takaful markets such as Saudi Arabia,

- the increasing integration of technology into takaful services with a view to improving accessibility and the customer experience,

- the rise of insurtech, which offers innovative digital solutions: mobile applications and online platforms,

- the widening scope of Islamic insurance markets with the diversification of products better suited to consumer needs: health, education and investment.

Read also | Takaful non-life insurance: technical ratios

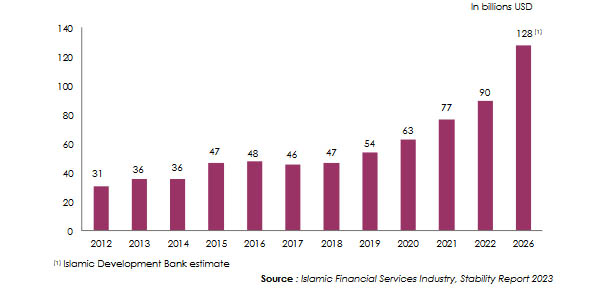

Takaful insurance market assets: 2012-2022

In Islamic finance, takaful insurance not only meets the expectations of policyholders, but it is also attracting the interest of investors. Sustainable development projects with social, ecological and ethical connotations are the main focus of investments initiated by takaful insurers.

The total value of assets built up over the past decade has tripled, rising from 31 billion USD in 2012 to 90 billion USD in 2022, representing an average annual growth of 12%. Projections point to 128 billion USD in assets generated by 2026.

Despite this growth, takaful assets account for only a tiny 2% of total Islamic finance assets, which, according to the Islamic Finance Development Report 2023, amounted to 4 500 billion USD in 2022.

Takaful insurance market: region-based assets

L’activité takaful est principalement localisée dans les pays membres de l'Organisation de Coopération Islamique (OCI).

In 2022, the regional breakdown of takaful assets showed strong concentration in three regions: MENA (excluding Gulf countries), Gulf Cooperation Council (GCC) countries and Southeast Asia. These three zones accounted for 83 billion USD in assets in 2022, representing a global share of 92%.

In millions USD

| Region | 2018 | 2020 | 2021 | 2022 |

| MENA (excluding GCC) | 13 | 19.877 | 30.08 | 40 |

| Gulf Cooperation Council countries (GCC) | 19 | 22.594 | 23.597 | 27 |

| Southeast Asia | 12 | 15.846 | 15.457 | 16 |

| South Asia | 1 | 1.322 | 2.106 | 5 |

| Europe | 1 | 2.402 | 1.637 | 2 |

| South America and the Caribbean | 0.001 | 4 | 4 | ND |

| Other countries | 0.004 | 0.04 | 0.04 | ND |

| Total | 46.005 | 66.081 | 76.917 | 90 |

(1) 2019 data not available

NA: Not available

Read also | Takaful family business

Takaful insurance market: country-based assets (2018-2022)

In descending order, the main takaful assets are to be found in the Iranian, Saudi and Malaysian markets. In 2022, these three countries alone recorded total assets under management of 74 billion USD, compared to 60 billion USD a year earlier and 37 billion USD in 2018.

In billions USD

| Country | 2018 | 2019 | 2020 | 2021 | 2022 |

| Iran | 13 | 14 | 20 | 30 | 39 |

| Saudi Arabia | 15 | 17 | 17 | 18 | 22 |

| Malaysia | 9 | 10 | 12 | 12 | 13 |

| United Arab Emirates | 3 | 3 | 3 | 3 | 3 |

| Indonesia | 3 | 3 | 4 | 3 | 3 |

| Turkey | 1 | 1 | 2 | 2 | 2 |

| Pakistan | 0.5 | 0.5 | 1 | 1 | 4 |

| Qatar | 1 | 1 | 1 | 1 | 1 |

| Bangladesh | 1 | 1 | 1 | 1 | 0.5 |

| Oman | - | - | - | 0.5 | 0.5 |

Source: Islamic Financial Services Industry, Stability Report 2023

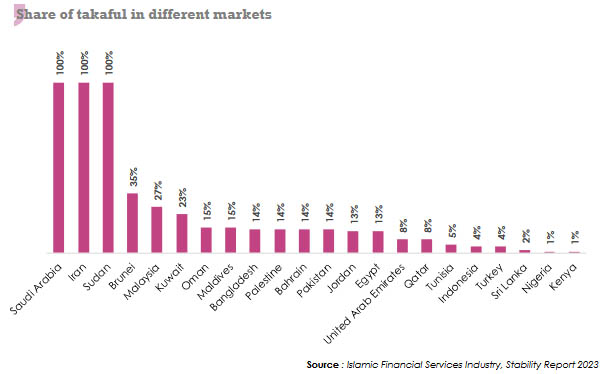

Takaful and conventional insurance

Only three markets - Iran, Saudi Arabia and Sudan - fully comply with Islamic insurance criteria. In many other markets, traditional insurance products rub shoulders with Sharia-compliant products.

The market shares of takaful insurance range from 100% (Saudi Arabia, Iran, Sudan) to 1% in Kenya and Nigeria, which have recently adopted the concept.

The takaful insurance market premium

Over the past 20 years, takaful premiums have gone sixteen-fold, rising from 2.1 billion USD in 2022 to 33.6 billion USD in 2023, the year when it accounted for a 12% increase in comparison with 2022.

According to the study "Takaful Market Report: Global Industry Trends, Share, Size, Growth, Opportunities and Forecast 2024-2032", the size of the global takaful market is poised to reach 74 billion USD in 2032, assuming an average annual growth rate of 8.9%.

Evolution of contributions: 2002-2023

In billions USD

| 2002 | 2008 | 2010 | 2011 | 2015 | 2017 | 2021 | 2022 | 2023 (1) | |

| Takaful premiums | 2.1 | 5.3 | 8.9 | 11 | 17 | 20 | 25.8 | 30 | 33.6 |

(1) Arab Monetary Fund estimates for 2023

Read also | Regulation of takaful insurance business

Takaful insurance market: turnover by region

As mentioned in previous developments, the highest takaful premiums in 2022 are found in the Gulf markets, accounting for 55.6% of total business. In fact, Saudi Arabia remains the growth driver for this industry in the Gulf.

The MENA zone (excluding GCC countries) and South-East Asia generated premiums of 6 billion USD and 5.9 billion USD respectively in the same year, each representing a market share of 20%.

Takaful insurers based in sub-Saharan Africa, Europe and the Americas account for just 4.4% of premium income in 2022.

Over the 2021-2022 period, the takaful insurance market as a whole grew by 16.3%. At 33.3%, Africa has the highest growth rate, followed by the GCC zone at 23.7%.

Premium breakdown by region: 2021-2022

In billions USD

| Region | 2021 | 2022 | 2021-2022 evolution |

| GCC | 14.5 | 16.7 | 23.7% |

| MENA (excluding GCC) | 5.7 | 6 | 5.3% |

| Southeast Asia | 5.5 | 5.9 | 7.3% |

| Africa | 0.6 | 0.8 | 33.3% |

| Others | 0.5 | 0.6 | 20.0% |

| Total | 25.8 | 30 | 16.3% |

Source : Islamic Financial Services Industry, Stability Report 2023

Takaful Insurance Market: turnover by country

The three leading takaful insurance markets - Saudi Arabia, Iran and Malaysia - account for almost 80% of global premiums. Among the top three, Saudi Arabia alone accounts for 47% of premiums in 2022.

2022 premium breakdown by country

In billions USD

| Country | 2022 contributions | 2022 shares | 2021-2022 growth |

| Saudi Arabia | 14.2 | 47.33% | 26.90% |

| Iran | 5.4 | 18.00% | 6.00% |

| Malaysia | 4.13 | 13.77% | 9.10% |

| Turkey | 0.647 | 2.16% | 57.10% |

| Qatar | 0.527 | 1.76% | 72.50% |

| Sudan | 0.488 | 1.63% | 78.00% |

| Egypt | 0.278 | 0.93% | 118.10% |

| Pakistan | 0.26 | 0.87% | 9.40% |

| Jordan | 0.116 | 0.39% | 15.00% |

| Brunei | 0.1145 | 0.38% | 6.90% |

| Palestine | 0.06 | 0.20% | 45.00% |

| Tunisia | 0.06 | 0.20% | 12.00% |

| Bahrain | 0.0231 | 0.08% | -4.9% |

| Maldives | 0.0118 | 0.04% | 29.40% |

| Other countries | 3.6846 | 12.28% | - |

| Total | 30 | 100% | 16.30% |

Source : Islamic Financial Services Industry, Stability Report 2023