As a protection mechanism designed for low-income individuals, microinsurance is often perceived as a difficult business to develop. The low cost of premiums and its low profitability deter many investors and operators from getting involved.

Despite this, the number of beneficiaries continues to grow globally, reaching approximately 344 million people in 2023 compared to 294 million in 2022.

The penetration rate of this sector remains very low, however, with only about 12% of the target population covered, indicating significant opportunities for growth, particularly in Africa, the Asia-Pacific region, and Latin America.

Definition of microinsurance

Microinsurance is a low-cost insurance plan based on affordable premiums tailored to the financial means of low-income individuals.

It is designed to protect populations, who are generally excluded from traditional insurance offerings, against certain risks such as illness, death, accidents, or natural disasters.

How microinsurance works

Microinsurance operates through a simple and inclusive mechanism: policyholders make regular small contributions which are pooled into a common fund. In the event of a loss, policyholders receive compensation or financial support from this fund. This system enables vulnerable populations to access basic financial protection at a low cost.

Microinsurance is often distributed through alternative channels, including microfinance institutions, cooperatives, non-governmental organizations (NGOs), and mobile solutions.

Overview of the global microinsurance market in 2025

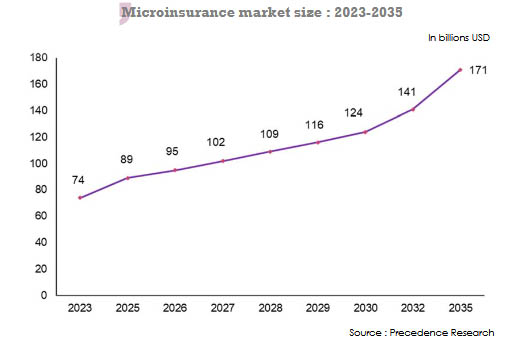

According to estimates by Precedence Research Firm, the microinsurance market reached 89.06 billion USD in 2025. With an average annual growth rate of 6.7%, the market is expected to reach 95 billion USD in 2026 and 171 billion USD by 2035.

This growth is particularly driven by increased smartphone penetration and the rise of mobile money, which facilitate the distribution of insurance solutions tailored to the needs of underserved or underinsured populations.

Key drivers of microinsurance growth

Digital innovation is the main driver of growth in microinsurance. This growth pertains to:

- the widespread recourse smartphones,

- automation of the underwriting process,

- rapid claims processing,

- the growing recourse to mobile and digital payment systems: payment platforms and e-wallets.

These technological advances enable vulnerable populations, who have limited access to traditional services, to underwrite low-cost, tailored policies that are accessible via digital applications.

In addition to technological progress, other factors also contribute to the development of microinsurance, such as:

- government programs and NGO efforts promoting the adoption of microinsurance through mobile banking and fintech platforms,

- increased public awareness of climate risks and the rise in natural disasters, which drives demand for crop, weather, and parametric insurance solutions in vulnerable regions,

- public-private partnerships: collaborations between insurers, microfinance institutions, and development agencies help increase the reach and penetration of microinsurance in low-income communities.

According to the study “State of Microinsurance in 2024,” published by the Micro Insurance Network (MiN) (1), the number of people covered by microinsurance in 37 countries reached approximately 344 million in 2023.

The agency estimates that approximately 88% of the target population remains uninsured, highlighting the sector’s strong growth potential.

(1) The Micro Insurance Network (MiN) is an international organization based in Luxembourg dedicated to promoting microinsurance and inclusive insurance.