The Origins of microinsurance in Africa

In Africa, microinsurance has developed gradually from informal solidarity mechanisms, such as tontines, mutual aid groups, and funeral societies, which provided coverage for certain risks.

Starting in the 1970s, more organized forms emerged with insurance cooperatives. In the 1980s, health mutuals developed, particularly in West Africa.

The mid-1990s marked a major milestone in the development of microinsurance with the arrival of private insurers. These insurers began designing products tailored to the needs of low-income populations, a trend driven by the rise of microfinance and strong demand for protection.

Since the late 1990s, microinsurance has become more structured through partnerships between insurers, microfinance institutions, and international organizations.

State of microinsurance in Africa

Microinsurance is gradually setting in as a driver of economic stability and financial security in Africa. This trend is reflected in strong market growth, estimated at approximately 4.5 billion USD by 2025, up from 756 million USD in 2014, according to estimates by the consulting firm IMARC Group.

The sector’s growth is driven by several factors, including the presence of a large low-income population, the gradual implementation of regulatory frameworks in several African countries, and the development and diversification of distribution channels, particularly digital ones.

It is worth noting that the COVID-19 health crisis has accelerated the adoption of these policies, particularly for the coverage of medical expenses.

On a continental scale, South Africa stands out as the leading player in this market.

Microinsurance: An economic opportunity

The African microinsurance market showcases significant growth potential in view of:

- the size of the population, which reached 1.47 billion by 2024,

- the high level of economic vulnerability among a large portion of the population; in West and Central Africa, 35.54% of the population lives below the extreme poverty line, set at 3 USD per day, while for all of Sub-Saharan Africa this proportion rises to 45.09% (1),

- the predominance of the informal sector in the economy. This sector accounts for more than 80% of jobs in many countries, with workers in this sector generally deprived of social protection or insurance,

- the low level of insurance coverage and the lack of specific mechanisms to protect vulnerable households.

In view of this situation, microinsurance is gradually emerging as a lever for financial inclusion.

(1) Source: The World Bank

Main microinsurance market trends in Africa

The microinsurance landscape in Africa is undergoing a structural transformation, marked by product diversification and the modernization of access channels.

Between 2014 and 2024, the sector has gradually shifted from niche solutions to more integrated models, driven by technological innovations and supportive public policies.

Digital distribution

The microinsurance ecosystem in Africa is increasingly relying on mobile technologies and digital solutions to simplify procedures and reduce management costs. This model promotes the inclusion of rural populations and self-employed workers, who have traditionally been excluded from traditional insurance channels.

In 2014, mobile network operators provided coverage to approximately one million people, through only five products (property damage, health, agricultural risks, credit, and personal accident insurance). This distribution channel accounted for only around 1% of microinsurance premiums (2).

The 2024 data confirm the growth of this distribution model: approximately 2.5 million people are now covered through mobile operators, mainly in life and health insurance. Their contribution to total microinsurance premium volume has now reached 2%, that is, twice as much compared with 2014.

(2) Source: Microinsurance Network Africa landscape.

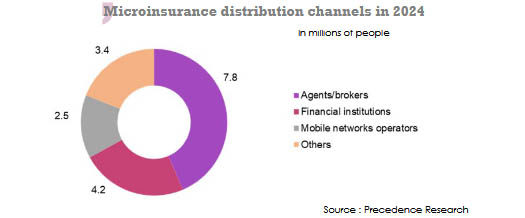

Evolution of distribution channels

In Africa, the distribution of microinsurance products is still largely dominated by agents and brokers, who account for nearly 34% of the collected premiums, covering several million beneficiaries. However, the sector is undergoing a gradual transformation driven by new digital technologies, particularly through the rise of fintechs and insurtechs.

These new players are developing innovative solutions based on artificial intelligence, remote sensing, and data analysis to improve risk assessment (index-based agricultural insurance) and claims processing (automated payment of compensation).

Partnerships with mobile operators, digital platforms, and community networks also promote a wider distribution of products to populations excluded from traditional insurance channels. This evolution reflects a growing trend towards a more digitized, accessible microinsurance that is tailored to the needs of vulnerable populations.

In terms of distribution, telecommunications operators rank third (covering 2.5 million people) after agents/brokers (7.8 million people) and financial institutions (4.2 million people covered).

Development of mobile payment

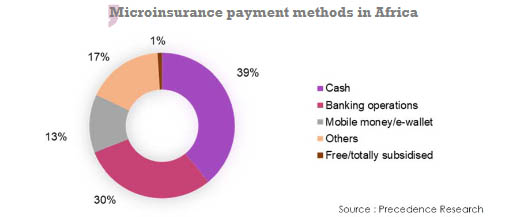

Payment methods are essential for the expansion of microinsurance. They are designed to facilitate the collection of premiums and the payment of claims through channels that are easily accessible for clients and viable for providers.

In 2024, mobile money and electronic wallets account for the third payment method for microinsurance products in Africa. These methods represent 13% of microinsurance transactions, behind cash payments (39%) and banking operations (30%).

Growth of embedded microinsurance

Microinsurance products are increasingly integrated into microfinance loans, associated with mobile payments, or included in everyday services (agriculture, telecommunications).

Generally, the integration of microinsurance coverage into another product is not mandatory. However, in practice, underwriting coverage may be required, therefore, purchased automatically, to access another financial service.

Climate and agricultural insurance

Agriculture is a pillar of the African economy, contributing 23% of the African GDP and employing nearly 60% of the population. In Sub-Saharan Africa, the agricultural sector accounts for nearly 55% of employment and 18% of the average regional GDP.

Africa is heavily affected by extreme climatic phenomena namely irregular rainfall, flooding, and rising temperatures, that threaten the viability of rural households dependent on natural resources.

In this context, agricultural insurance, covering crops and livestock, emerges as a key product in microinsurance, with offers increasingly incorporating coverage against climatic risks.

(1) Selon les données 2024 de la Banque Mondiale.

The evolution of agricultural microinsurance in Africa

| Number of agricultural products | Number of insured persons | Coverage rate | |

| 2024 | 47 | 2.3 millions | 0.6% |

| 2014 | 25 | 1.1 million | 0.1% |

Source: Microinsurance Network Africa landscape

Despite the advancement of agricultural microinsurance, penetration remains very low, with only 0.6% of the target population reached. Furthermore, out of 47 agricultural insurance products available in 2024, 36 receive some level of subsidy.

Key products developed by microinsurance market in Africa

According to the Landscape of Microinsurance study conducted in 15 African countries, funeral insurance constitutes the primary line of business for individual microinsurance in Africa, due to its strong historical presence in Southern Africa. It covers 17.3 million people, including 9.6 million in Zimbabwe and 7.2 million in South Africa. Life and accident products collectively cover nearly 28 million people, with an estimated premium volume of 0.3 billion USD.

Additionally, property damage and loss of income insurance protect 6.7 million people, generating 34 million USD in premiums in 2023, accounting approximately for 1.4% of the target population.

Finally, the health insurance business covers 4.5 million individuals. Although it reaches only about 1.9% of the target population, it represents a market share estimated at 0.8%.

Financial inclusion and coverage of the informal sector

Microinsurance is progressively setting in as a major lever for financial inclusion, facilitating access for low-income populations to formal risk protection mechanisms.

It, therefore, contributes to integrating households traditionally excluded from conventional banking and insurance services into the financial system, particularly informal sector workers, small farmers, and micro-entrepreneurs. By offering low-cost products tailored to the capacities of vulnerable populations, microinsurance helps reduce the "protection gap," meaning the gap between the risks actually faced and the levels of available coverage.

Conclusion

The microinsurance market in Africa is experiencing sustained growth dynamics, driven by the rise of digital solutions, the widespread recourse to mobile money, and the development of products tailored to the needs of vulnerable populations.

This evolution confirms the emergence of an increasingly structured and attractive sector, particularly for insurers and investors. Despite this breakthrough, the penetration level of microinsurance remains very low compared to the market's potential. Furthermore, the market is required to come to grips with regulatory reforms, climatic volatility, emerging technologies, and increasing socio-economic inequalities.

Major African microinsurance players

| Companies | Country | Products | Coverage | Number of beneficiaries |

| Hollard Insurance | South Africa | Pep Stores | Burial insurance | More than 600 000 policyholders |

| Ghana | MeBanbó | Funeral and disability microinsurance | ||

| Mozambique | ||||

| Wafacash | Morocco | Taamine iktissaadi: Taamine Al Janaza, Wladi, Al Walidine, Sahti, Bayti, Mahali | Health, funeral, and family microinsurance | In 2023, more than 565 000 people were covered and more than 1 670 claims were paid |

| GOXI Microinsurance | Nigeria | GOXI Family Shield | Life and health insurance | More than 532 000 people covered from 2019 to 2024 |

| Nassure Microinsurance | Nigeria | Cuva | Life, provident, funeral, and credit insurance | |

| CHI Microinsurance | Nigeria | Group insurance / PLAN ESUSU | Cooperative credit insurance, project/home savings, provident insurance, group life insurance | |

| YES Microinsurance | Nigeria | 4 microinsurance products | Life, credit, bodily injury, microgroup life, and funeral insurance | |

| Sawa Micro-insurance Co. | Egypt | In the launch phase | The first licensed microinsurance company in Egypt | |

| Britam Connect | Kenya | Kinga Ya Mkulima, integrated insurance | Health, bodily injury and flood insurance | More than 4 million Kenyans were covered in 2024, including 200 000 farmers and 300 000 self-employed workers |

| SAMB’A Assurances | Gabon | Company founded in 2024 | Life, property, group, and agricultural insurance | |

| SAMB’A Assurances | Cameroon | In the launch phase | Bodily injury, health, agriculture, property damage, and death insurance |